Buying A Primary Home Versus Second Home In Santa Rosa Beach

Are you picturing sunsets on 30A and wondering if Santa Rosa Beach should be your everyday address or your getaway spot? You are not alone. Many buyers weigh the lifestyle benefits against financing, taxes, insurance, and rental rules before choosing a path. In this guide, you will see the key differences, the neighborhoods that fit each goal, and a simple checklist to make a confident choice. Let’s dive in.

Mortgage rules change based on how you will use the home.

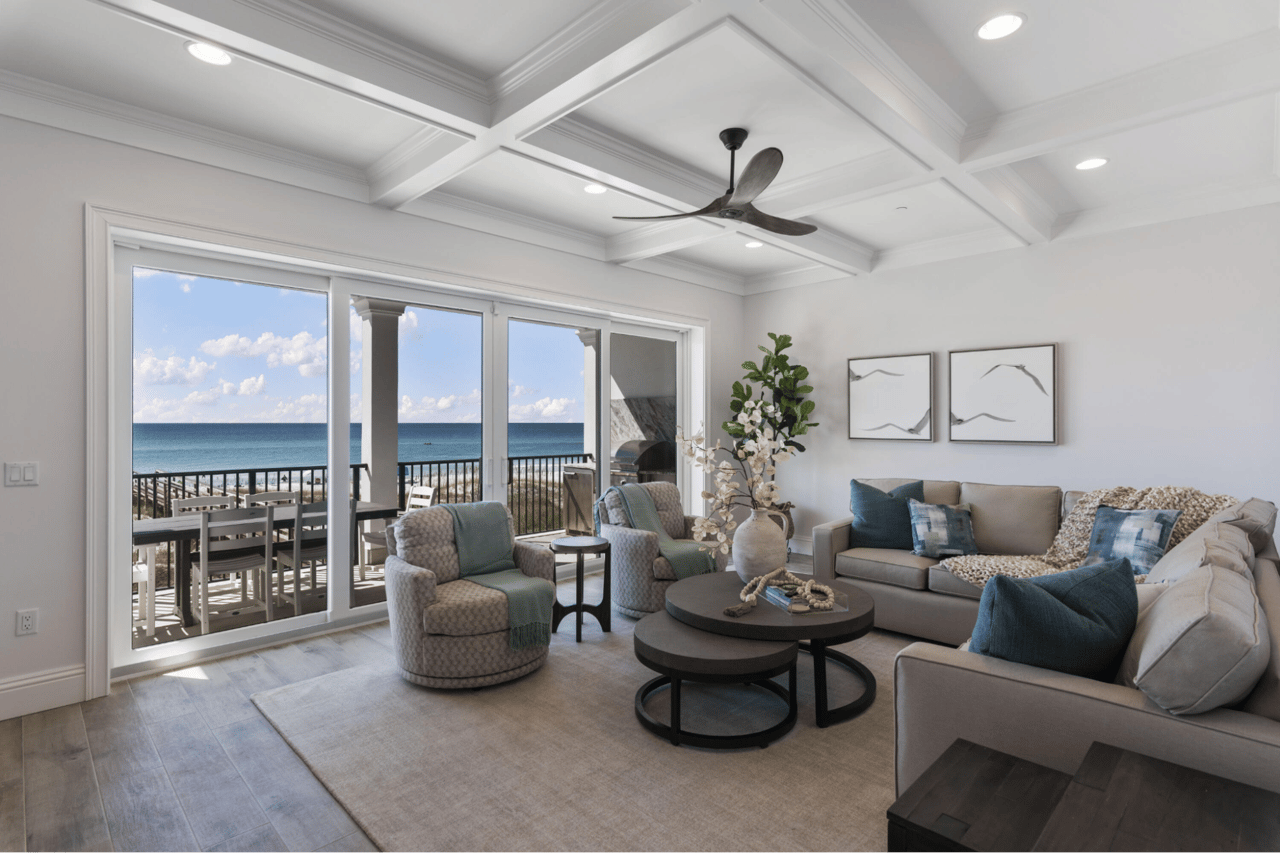

Santa Rosa Beach spans inland neighborhoods and the walkable 30A corridor. Micro-location and adjacency to the Gulf drive pricing and rental dynamics. A home a few blocks off 30A can perform very differently than a gulf-front property in the same ZIP code.

If you plan to rent your second home when you are not using it, factor in compliance, seasonality, and operating costs.

Use this pre-offer checklist to reduce surprises and keep your deal on track:

Ready to map your options and tour properties that match your plan? Connect with the native Emerald Coast team at Abbott Martin Group for tailored guidance and on-the-ground insight.

It is essential to love the people you work with, and that indeed is the case within our team, where culture comes first. At Abbott Martin Group, we celebrate success and pick each other up when needed. A strong culture is vital to having a healthy work environment. We focus on creating a positive impact for our families and the customers we serve. The Emerald Coast is an environment of healing; we are always here for each other.

Stay up to date on the latest real estate trends.

June 26, 2026

What Miramar Beach Buyers Need to Budget for Beyond the Purchase Price.

June 26, 2026

Discover Which Miramar Beach Neighborhood Fits Your Lifestyle and Investment Goals.

May 8, 2026

How the Age of a Property Shapes Pricing, Buyer Perception, and Long-Term Investment Value Along the Emerald Coast.

May 8, 2026

What Every Seller Needs to Know Before Listing on the Emerald Coast.

May 1, 2026

Proven Strategies for Reaching the Right Buyers Wherever They Are.

May 1, 2026

What Every Discerning Buyer Should Know Before Closing on the Emerald Coast.

We pride ourselves in providing personalized solutions that bring our real estate clients in Miramar Beach closer to their dream properties and enhance their long-term wealth. Contact us today to find out how we can assist you!